How to Salary Sacrifice Super: A Practical Guide for Australians

- 바른회계법인

- Jan 10

- 8 min read

Salary sacrificing into your superannuation is a powerful, tax-effective strategy for building your retirement savings while potentially reducing your current income tax. It is a formal arrangement with your employer to direct a portion of your pre-tax salary straight into your super fund.

This arrangement matters because it can significantly accelerate your retirement savings. Instead of your full salary being taxed at your marginal income tax rate, the sacrificed portion is channelled directly to your super and taxed at a lower concessional rate. This dual benefit lowers your taxable income for the financial year and boosts the amount of money compounding in your super fund.

However, non-compliance with Australian Taxation Office (ATO) rules carries significant risks. An ineffective arrangement or exceeding annual contribution caps can lead to penalties that negate the tax benefits. This guide provides a clear, step-by-step process to ensure your salary sacrifice strategy is both effective and compliant.

What is Salary Sacrifice into Super?

Salary sacrifice is an arrangement where an employee agrees to forgo part of their future pre-tax salary in return for their employer providing benefits of a similar value. When applied to superannuation, it means directing a portion of your earnings into your super fund before income tax is calculated. These contributions are in addition to the compulsory Superannuation Guarantee (SG) payments your employer is required to make.

The primary advantage is tax efficiency. Income paid to you is taxed at your marginal rate, which can be up to 47% (including the Medicare levy). In contrast, salary sacrificed contributions are classified as concessional contributions.

The Power of Lower Tax Rates

Once inside your super fund, concessional contributions are typically taxed at a flat rate of 15%. For most individuals, this is a significant tax saving compared to their personal income tax rate.

This tax differential delivers two key benefits:

Reduced Taxable Income: By lowering your gross salary, you reduce the total income assessed by the ATO, potentially lowering your overall income tax liability for the year.

Boosted Super Balance: A larger portion of your earnings enters your retirement fund because less is lost to tax. This allows more capital to be invested and benefit from compound growth.

A crucial point from the ATO: an effective salary sacrifice arrangement must be established before the work is performed. It cannot be applied retrospectively to salary or wages you have already earned.

Salary Sacrifice Tax Savings at a Glance

This table illustrates the potential annual tax savings for an individual sacrificing $5,000 of their pre-tax income into super across different income brackets for the 2024-25 financial year.

Annual Income | Marginal Tax Rate (incl. Medicare Levy) | Tax on $5,000 as Income | Tax on $5,000 as Super Contribution | Potential Annual Tax Saving |

|---|---|---|---|---|

$60,000 | 34.5% | $1,725 | $750 | $975 |

$100,000 | 34.5% | $1,725 | $750 | $975 |

$150,000 | 39% | $1,950 | $750 | $1,200 |

$200,000 | 47% | $2,350 | $750 | $1,600 |

Note: Individuals with income and concessional contributions exceeding $250,000 may be subject to Division 293 tax, which applies an additional 15% tax on some or all of their contributions.

ATO Compliance and Contribution Caps

The ATO strictly regulates superannuation contributions. Salary sacrifice payments are classified as concessional contributions. These, along with your employer's SG payments and any personal deductible contributions, are subject to an annual cap. Exceeding this cap can trigger additional tax and penalties, negating the benefits. For more information on tax obligations, you might find our guide on how to get your PAYG payment summary helpful.

A Step-by-Step Guide to Setting Up Salary Sacrifice

Implementing a salary sacrifice arrangement is a structured process that requires clear communication with your employer and adherence to ATO regulations.

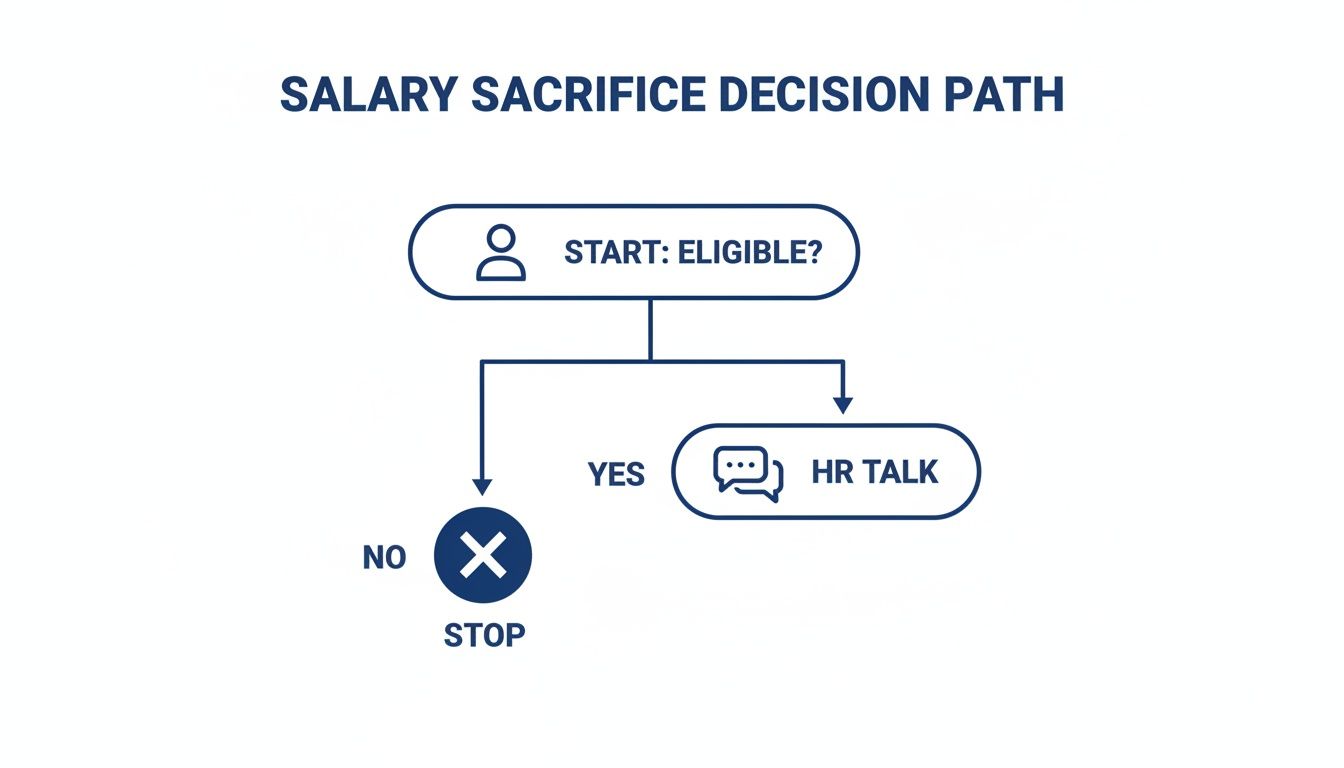

Step 1: Confirm Eligibility and Company Policy

Before proceeding, confirm that your employer offers salary sacrifice arrangements. While most do, it is not mandatory. Contact your HR or payroll department to verify their policy and understand any specific internal procedures or forms they require.

Step 2: Calculate Your Contribution Amount

Determine how much you can afford to contribute from your pre-tax salary. Critically, you must calculate your available space under the annual concessional contributions cap. Annual Cap - Employer SG Contributions = Your Available Cap Space This ensures you do not accidentally exceed the limit.

Step 3: Initiate the Request with Your Employer

Formally request to set up the arrangement. A clear, written request is essential.

You can use this template:

Subject: Enquiry regarding a salary sacrifice arrangement for superannuation Dear [HR/Payroll Manager's Name], I am writing to establish a salary sacrifice arrangement to make additional concessional contributions to my superannuation fund. I would like to arrange to sacrifice [a fixed amount of $XXX per pay period / X% of my pre-tax salary] into my nominated super fund, effective from the next full pay period. Could you please advise on the process and provide any necessary documentation to formalise this agreement? Thank you, [Your Name] [Employee ID]

Step 4: Formalise the 'Effective Salary Sacrifice Arrangement'

The ATO requires a formal, written agreement to be in place before you perform the work for which the salary is earned. A verbal agreement is insufficient for compliance.

An 'effective salary sacrifice arrangement' (SSA) must:

Be in writing to provide a clear record for you, your employer, and the ATO.

Apply only to future earnings. It cannot be backdated.

Clearly state the terms, including the amount being sacrificed per pay period and the duration of the agreement.

For a detailed analysis of the advantages, see our guide on the core benefits of salary sacrificing.

Navigating Contribution Caps and ATO Rules

Managing your salary sacrifice arrangement effectively means staying within the ATO's contribution limits. The most important rule relates to the annual concessional contributions cap.

The cap is the total limit for all tax-advantaged contributions to your super in a financial year, including:

Your employer's mandatory Superannuation Guarantee (SG) payments.

Your salary sacrifice contributions.

Any personal contributions for which you claim a tax deduction.

For the 2024-25 financial year, the general concessional contributions cap is $30,000. This figure is indexed periodically, so it's essential to verify the current cap each year on the ATO website.

This flowchart outlines the initial decision-making process.

Calculating Your Available Cap Space

Before committing to a sacrifice amount, calculate how much "space" you have left under the annual cap. This is a critical step to avoid penalties.

Example: An individual earning $120,000 per year in the 2024-25 financial year.

The SG rate is 11.5%.

Employer SG contribution: $120,000 x 11.5% = $13,800.

Available cap space: $30,000 (annual cap) - $13,800 (SG) = $16,200. This individual can contribute up to $16,200 through salary sacrifice or personal deductible contributions for the year.

Using Carry-Forward Concessional Contributions

The ATO provides a 'carry-forward' provision for unused cap amounts.

If your total super balance was less than $500,000 on 30 June of the previous financial year, you may be able to contribute more than the annual cap by using unused amounts from the previous five financial years.

This is particularly useful for individuals who have had career breaks, worked part-time, or wish to make large contributions after receiving a bonus. Your available carry-forward balance can be viewed in your myGov account linked to the ATO.

Penalties for Exceeding the Cap

If your contributions exceed the cap, the excess amount is included in your assessable income and taxed at your marginal rate. You will also be liable for an excess concessional contributions charge (an interest penalty). This effectively nullifies the tax benefit. Diligent tracking of all contributions is non-negotiable.

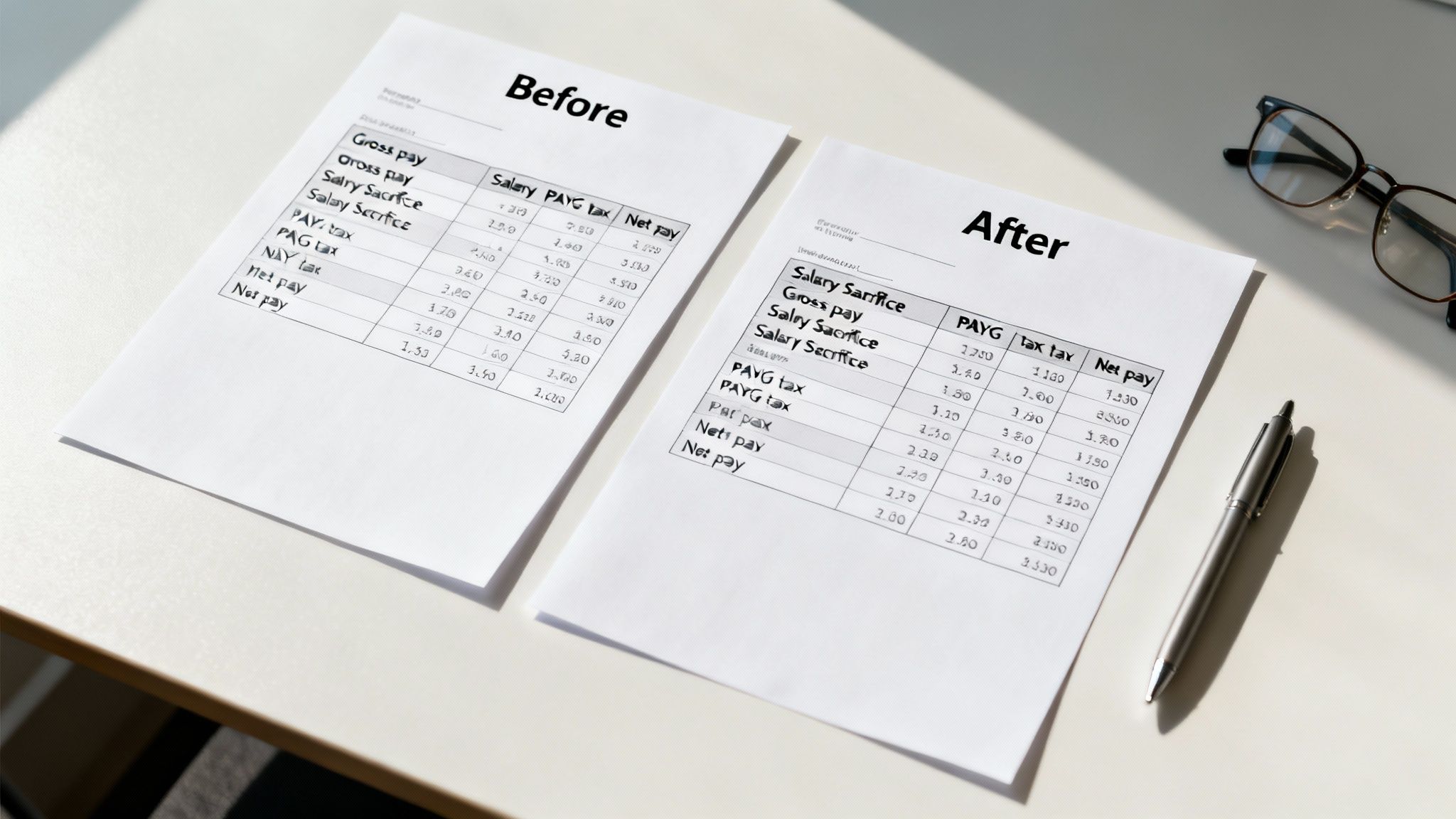

Practical Example: How Salary Sacrifice Impacts Your Payslip

Understanding how this arrangement appears on your payslip clarifies its financial impact. Your employer deducts the sacrificed amount from your gross salary before calculating Pay As You Go (PAYG) tax. This reduces your taxable income for the pay period, resulting in less tax withheld.

Before vs After Payslip Comparison

Let's consider an employee, David, earning $90,000 per year who decides to salary sacrifice $500 per fortnight.

Gross Fortnightly Pay: $90,000 / 26 = $3,461.54

SG Contribution (11.5%): $3,461.54 x 11.5% = $398.08

Payslip Item | Before Salary Sacrifice | After Salary Sacrifice |

|---|---|---|

Gross Pay | $3,461.54 | $3,461.54 |

Pre-Tax Sacrifice | $0.00 | -$500.00 |

Taxable Income | $3,461.54 | $2,961.54 |

PAYG Tax Withheld | -$782.00 | -$617.00 |

Net (Take-Home) Pay | $2,679.54 | $2,344.54 |

Total Super Input | $398.08 (SG only) | $898.08 (SG + Sacrifice) |

Analysis of the Impact:

David's fortnightly take-home pay decreases by $335.00.

His superannuation fund receives an additional $500.

The net cost to his take-home pay is only $335 to secure a $500 retirement contribution, thanks to an immediate tax saving of $165 for that pay period.

Common Pitfalls and How to Avoid Them

While effective, salary sacrifice arrangements are prone to common errors that can undermine their benefits. Awareness and proactive monitoring are key to avoiding them.

Checklist for Avoiding Common Errors:

[ ] Verify Correct SG Calculations: * Pitfall: Some employers incorrectly reduce their SG payment obligation by using the employee's sacrificed amount. The SG must be calculated on your reduced cash salary. * Solution: Check your payslip to ensure both the employer SG contribution and your separate salary sacrifice contribution are clearly listed.

[ ] Confirm Contributions are Paid: * Pitfall: An employer deducts the amount from your pay but fails to transfer it to your super fund in a timely manner (or at all). Legally, they must pay super at least quarterly. * Solution: Regularly log in to your super fund's online portal to verify that contributions shown on your payslip have been received.

[ ] Monitor the Annual Contribution Cap: * Pitfall: Receiving a pay rise, bonus, or changing jobs mid-year can lead to unintentional excess contributions as your SG payments increase. * Solution: Recalculate your total expected contributions whenever your income changes. Adjust your salary sacrifice amount accordingly to stay under the cap. This is also relevant when dealing with other employer-provided benefits; see our guide on how to manage Fringe Benefits Tax (FBT) in Australia.

[ ] Understand Impact on Other Calculations: * Pitfall: Forgetting that sacrificed amounts are added back to your income for certain government tests. * Solution: Be aware that your 'adjusted taxable income' (which includes sacrificed amounts) is used to assess HECS-HELP repayments, eligibility for Family Tax Benefit, and the Medicare Levy Surcharge. Factor this in during financial planning.

Frequently Asked Questions (FAQ)

1. Can casual and part-time employees salary sacrifice into super?

Yes. Eligibility is not determined by your employment status (full-time, part-time, or casual) but by your employer's policy. The same ATO rules apply: the arrangement must be agreed upon in writing before the income is earned. Casual employees should be particularly diligent in tracking their total contributions against the annual cap, as their income may fluctuate.

2. What happens if my employer doesn't pay my sacrificed super on time?

Your employer is legally required to pay superannuation contributions, including sacrificed amounts, to your nominated fund at least quarterly. If your payslip shows a deduction but the money has not appeared in your super account after the quarterly due date, you should first contact your employer's payroll department. If the issue is not resolved, you can report it to the ATO. According to the ATO, unpaid super can be investigated and recovered. You can find more information directly from the ATO for unpaid super.

3. Can I salary sacrifice if I have more than one employer?

Yes, you can establish a salary sacrifice arrangement with one or both employers. However, you are responsible for ensuring your total concessional contributions from all sources do not exceed the annual cap. This requires careful coordination and tracking of SG payments and salary sacrifice amounts from each employer to avoid penalties.

4. How do I stop or change my salary sacrifice arrangement?

You can change or cease your arrangement at any time, subject to the terms of your agreement with your employer. Any changes must be documented in writing and can only apply to future earnings. You cannot retrospectively alter contributions for work already performed. It is best practice to provide your employer with reasonable notice (e.g., one pay cycle) to ensure their payroll system is updated correctly.

Summary: Key Takeaways

Tax-Effective Strategy: Salary sacrificing reduces your taxable income by redirecting pre-tax salary to your super, where it is concessionally taxed at 15%.

Formal Agreement is Essential: You must have a legally 'effective salary sacrifice arrangement' in writing with your employer before you earn the income.

Monitor Contribution Caps: Your salary sacrifice amounts, combined with employer SG payments, must not exceed the annual concessional contributions cap ($30,000 for 2024-25) to avoid penalties.

Verify Payments: Regularly check your super fund account to confirm that contributions deducted by your employer have been paid correctly and on time.

Proactive Management: Adjust your arrangement if your income changes (e.g., pay rise, bonus) to ensure you remain compliant and maximise the benefits.

Seek Professional Advice

This article provides general guidance on how to salary sacrifice into super. However, individual financial circumstances vary. It is recommended to seek personalised advice from a qualified financial advisor or accountant to ensure this strategy aligns with your personal financial goals and retirement plan.

Contact Us

Baron Tax and Accounting

Website: https://www.baronaccounting.com

Email: info@baronaccounting.com

Phone: +61 1300 087 213

Comments