How Do Property Tax Deductions on a Rental Property Work in Australia?

- 바른회계법인

- Jan 10

- 13 min read

As a property investor in Australia, you can claim property-related taxes such as council rates and land tax against your rental income. These are considered standard running costs and are fully deductible in the financial year you pay them, provided your property was tenanted or genuinely available for rent during that period. Understanding these rules is crucial for compliance with the Australian Taxation Office (ATO) and maximising your investment returns.

Misclaiming deductions is a significant compliance risk. The ATO closely scrutinises rental property claims, and errors can lead to audits, amendments to your tax returns, and financial penalties. Ensuring your claims are accurate and substantiated is non-negotiable for any landlord.

Understanding Your Rental Property Tax Deductions

Navigating the long list of potential investment property expenses can feel daunting. However, a clear understanding of what you can and cannot claim is the first step to optimising your financial outcomes. Think of your rental property as a small business—the legitimate costs incurred to operate it can directly reduce your taxable income, increasing your net return.

Correctly classifying and claiming these deductions is essential. The Australian Taxation Office (ATO) maintains a strong focus on rental property claims, making adherence to their guidelines vital to avoid compliance issues.

The Three Core Types of Rental Expenses

To simplify the process, the ATO categorises rental property deductions into three main types. Identifying which category an expense falls into determines precisely when and how you can claim it.

Immediate Deductions (Expenses Claimed Now): These are your ongoing operational costs. You claim the full amount in the same financial year you incurred the expense. This includes council rates, land tax, loan interest, insurance, and property management fees.

Deductions Over Several Years (Expenses Claimed Over Time): Certain expenses provide a long-term benefit and must be claimed over several years. This category includes borrowing expenses paid to set up your loan (e.g., application fees) and capital works, such as significant renovations or structural improvements.

No Immediate Deduction (Expenses that Form the Cost Base): Some costs cannot be claimed as an immediate deduction. Instead, they are added to the property's "cost base." This is critical when you eventually sell the property, as a higher cost base reduces your assessable capital gain. These expenses include stamp duty, conveyancing fees, and the cost of initial repairs to rectify defects present at the time of purchase.

The Scale and Importance of Correct Claims

The number of Australian investors claiming rental deductions highlights the importance of accurate reporting. In recent years, millions of property investors have lodged claims, representing a significant component of the national economy.

ATO data consistently shows a discrepancy between the deductions claimed by self-preparing individuals and those prepared by qualified tax professionals. This suggests many investors may be unintentionally missing out on legitimate deductions or making incorrect claims, exposing them to compliance risk.

Correctly classifying expenses is a cornerstone of a sound investment strategy. For instance, claiming all eligible deductions may result in a net rental loss for the year, a strategy known as negative gearing. To understand this concept further, see our guide on mastering negative gearing tax benefits in Australia.

Ultimately, a thorough understanding of these rules ensures you claim every dollar you are entitled to without raising red flags with the ATO.

What You Can Claim Immediately on Your Rental Property

As a property investor, immediate deductions offer the most direct tax benefit. These represent the day-to-day running costs of your investment property. You can claim the full amount of these expenses against your rental income in the same financial year they are paid, which provides an immediate reduction in your taxable income.

The foundational rule, as stipulated by the ATO, is that the expense must relate to the period when your property was either rented out or genuinely available for rent. If the property was only available for part of the year, you must apportion the expenses accordingly.

Core Property Running Costs

These are the essential bills associated with property ownership. The ATO considers them direct operational costs, making them straightforward deductions.

Council and Water Rates: Payments made to your local council for rates are fully deductible. The same applies to service charges for water and sewerage. However, the cost of water consumption by your tenants is generally not deductible unless your tenancy agreement requires you to pay for it.

Land Tax: This is a state-based tax levied on the unimproved value of the land you own. It is an annual expense and is deductible in the year it is paid.

Body Corporate and Strata Fees: For owners of units, townhouses, or apartments, regular administrative and sinking fund levies paid to the body corporate are deductible. Note that special levies raised for major capital works (e.g., a full roof replacement) are treated as capital expenses and are generally not immediately deductible.

A crucial point from the ATO: It's not enough to just have a receipt. To claim a deduction, you must have actually incurred and paid the expense, and it has to be directly linked to earning your rental income.

Finance and Management Expenses

The costs associated with financing and managing your investment are often among the most significant deductions. For many investors, these expenses constitute the largest portion of their total claims.

Interest on Your Investment Loan

The interest charged on the loan used to purchase the rental property is typically the single largest tax deduction for investors. You can claim the interest component of your loan repayments, but not the principal portion, which reduces your loan balance.

It is critical that the loan was used solely for the investment property. If you redraw funds from the loan for private purposes, such as buying a car or funding a holiday, you must apportion the interest. Only the portion of the interest that relates to the investment can be claimed.

Property Manager and Letting Fees

Engaging a real estate agent to manage your property is a common business decision, and the associated costs are deductible. This includes:

Management Fees: The ongoing percentage of rent charged by your agent.

Letting Fees: The one-off fee for sourcing and placing a new tenant.

Advertising Costs: Expenses incurred to advertise the property for rent.

These are all direct costs of earning rental income and are fully deductible in the year they are paid. For a more detailed explanation of other finance-related claims, refer to our guide on claiming borrowing expenses.

Insurance and Other Operational Costs

Protecting your asset and maintaining its condition involves several other key expenses that you can claim immediately.

Insurance Premiums: Landlord insurance, building insurance, and contents insurance (for any items you own within the property) are all deductible.

Pest Control: The cost of regular pest inspections and treatments.

Gardening and Lawn Mowing: Fees paid for the maintenance of lawns and gardens.

Cleaning: Costs for professional cleaning, typically at the end of a tenancy.

Administrative Costs: Minor expenses such as stationery, postage, and phone calls directly related to managing the rental can also be claimed.

Meticulous record-keeping for every expense is mandatory to substantiate your claims and satisfy ATO requirements.

Repairs, Maintenance, and Capital Improvements Explained

This is an area where property investors frequently make errors, and it is subject to close ATO scrutiny. Distinguishing between a 'repair' (immediately deductible) and a 'capital improvement' (claimed over time) is critical. An incorrect classification can lead to an improper claim and potential ATO penalties.

The primary difference lies in the timing of the deduction. A repair is claimed in full in the financial year it occurs. An improvement is a capital expense and is claimed over many years.

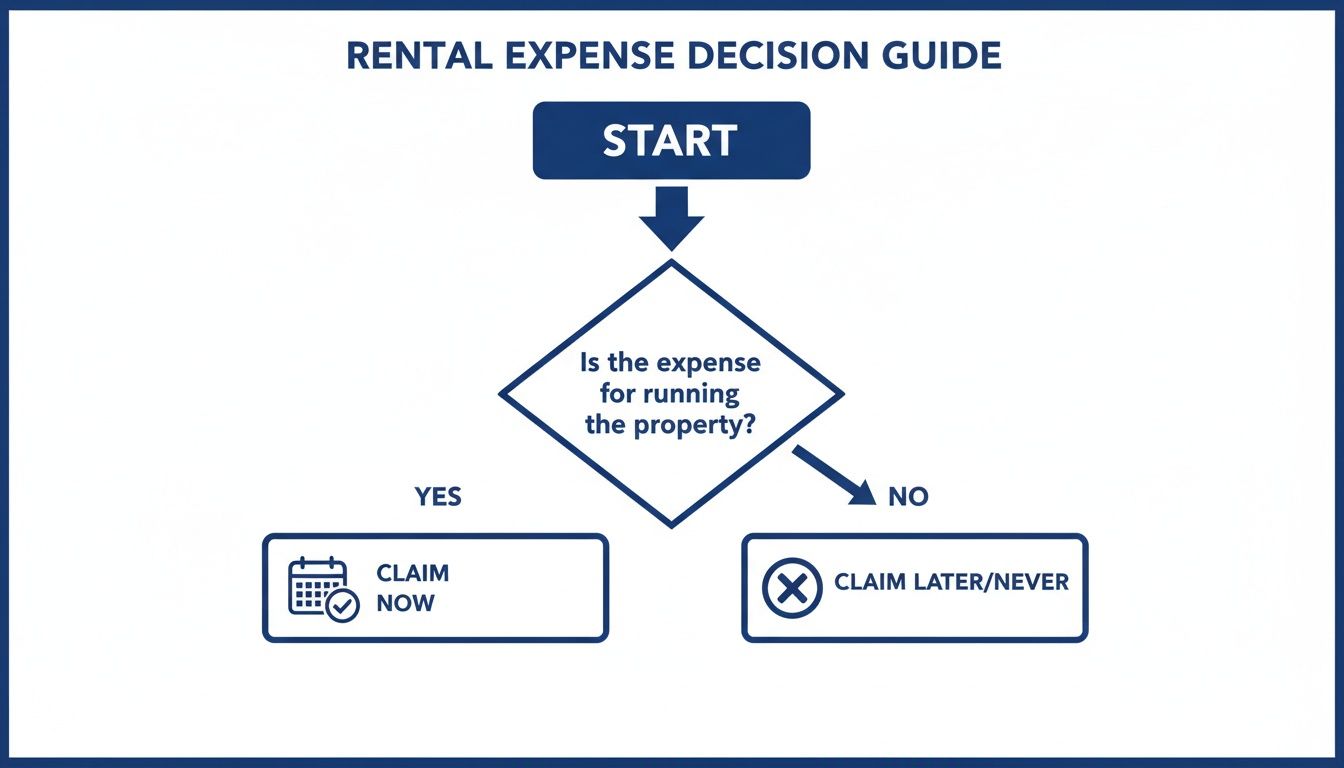

Let’s clarify the distinction.

This flowchart outlines the decision-making process for classifying an expense correctly, determining if you can claim it now, over time, or as part of the property's cost base.

Ultimately, the purpose of the expenditure—whether it was to restore the asset or enhance it—dictates its tax treatment.

Defining Repairs and Maintenance

The ATO defines a repair as work to remedy deterioration or damage. The objective is to restore an item to its original condition, not to improve it beyond its state when acquired.

Maintenance, conversely, is preventative work to stop deterioration or defects from occurring.

Examples of immediately deductible repairs and maintenance include:

Replacing a cracked pane of glass in a window.

Hiring a plumber to fix a leaking tap.

Repairing a faulty stove element.

Servicing an air conditioning unit to maintain its function.

Repainting a damaged section of a wall with the same quality paint.

Understanding Capital Improvements

A capital improvement is fundamentally different from a repair. It involves work that enhances the property's value, improves its functionality, or extends its useful life. In essence, you are upgrading the asset.

As the ATO states, "an improvement is anything that makes part of the property better, more valuable, more desirable or changes its character." Using materials of a higher quality than the original also constitutes an improvement.

These costs are not immediately deductible. They are classified as capital works and must be depreciated over their effective life, typically at a rate of 2.5% per year for 40 years for the building structure.

Common examples of capital improvements include:

A full renovation of a kitchen or bathroom.

Adding a new deck or pergola.

Replacing a tin roof with modern tiles.

Installing a new air conditioning system where one did not previously exist.

Repair vs Capital Improvement: A Practical Comparison

This table provides real-world scenarios to illustrate the difference between these categories.

Expense Scenario | Classification | ATO Treatment | Justification |

|---|---|---|---|

Replacing a few broken roof tiles after a storm. | Repair | 100% Deductible in the current year. | You are restoring the roof to its previous functional state. |

Replacing the entire roof with new, superior materials. | Capital Improvement | Depreciated over 40 years (at 2.5% per year). | You have upgraded the asset and improved its overall character. |

Repainting a single wall damaged by a tenant. | Repair | 100% Deductible in the current year. | This is a minor fix to restore the property's appearance. |

Repainting the entire interior immediately after purchase. | Initial Repair / Capital | Added to the property's cost base. | This improves the asset from the condition it was in when acquired. |

Fixing the motor in an existing air conditioning unit. | Repair | 100% Deductible in the current year. | You are repairing a component to restore the unit's function. |

Installing a brand-new, more efficient air conditioning system. | Capital Improvement | Depreciated over its effective life. | This is a significant upgrade that adds value and functionality. |

This comparison shows that the scale and purpose of the work are the key determinants for the ATO.

Initial Repairs: A Common Trap for New Landlords

A significant pitfall for new investors is the concept of initial repairs. This refers to work performed to fix defects, damage, or deterioration that existed at the time of purchase.

For example, if you bought a property with a dilapidated fence and replaced it shortly after settlement, this cost cannot be claimed as an immediate deduction. The ATO considers this a capital expense because it improves the asset from the condition in which it was acquired.

These costs are not lost; they are added to the property’s cost base, which helps reduce your Capital Gains Tax upon future sale.

Unlocking Value with Depreciation and Capital Works Claims

While deductions for ongoing expenses like council rates are claimed annually, some of the most substantial tax benefits are claimed over the long term. These deductions are spread over many years, systematically reducing your taxable income throughout your ownership of the investment.

These claims fall into two main categories, governed by the ATO under Division 43 (capital works) and Division 40 (depreciating assets). Understanding these is key to maximising the financial performance of your property.

Capital Works: The Building's Structure

Capital works deductions (Division 43) relate to the building's structure and permanently fixed items. This includes the original construction cost of walls, floors, roofs, foundations, and built-in fixtures.

This deduction allows you to claim the wear and tear on the building itself. For most residential properties constructed after 15 September 1987, you can claim a deduction of 2.5% of the construction cost each year for a maximum of 40 years.

For example, if your property’s original construction cost was $400,000, you could be eligible to claim a $10,000 deduction annually. This significantly reduces your taxable rental income.

Importantly, this is a "non-cash" deduction. You do not need to spend money in a given year to claim it. It is a deduction on paper that reflects the building's depreciation, but it delivers real tax savings. For more detail, refer to our guide on depreciation on an investment property.

Depreciating Assets: Items Within the Building

Depreciating assets (Division 40) are removable items within the property, often referred to as "plant and equipment." These assets have a limited effective life and lose value over time.

You can claim a deduction for the decline in value of assets such as:

Carpets and blinds

Ovens, cooktops, and rangehoods

Dishwashers and air conditioners

Hot water systems

Smoke alarms

Each asset has an "effective life" determined by the ATO, and the deduction is claimed over that period. For instance, a carpet may have an effective life of 10 years, while a dishwasher may have one of 8 years.

The 2017 Rule Change for Depreciating Assets

A significant legislative change took effect on 9 May 2017. If you purchased a residential rental property after this date, you can no longer claim depreciation on second-hand or previously used plant and equipment that came with the property.

This means for an established property, you cannot claim depreciation on the existing oven, carpets, or air conditioner. However, if you purchase and install a brand-new asset yourself, such as a new dishwasher, you are entitled to claim depreciation on that new asset.

The Role of a Quantity Surveyor

Determining the original construction cost of an older building or valuing every individual fixture is a complex task. This is where a qualified quantity surveyor is invaluable.

These professionals specialise in construction costing. They inspect your property and prepare a comprehensive tax depreciation schedule. This report separates the capital works value from the plant and equipment items, assigning a value and an effective life to each, which provides a clear basis for your claims for up to 40 years.

The fee for this report is tax-deductible, and it often unlocks thousands of dollars in legitimate deductions that would otherwise be missed.

Ensuring Compliance: Apportionment and Record-Keeping

When assessing rental property deductions, the ATO operates on two fundamental principles. First, you can only claim the portion of an expense that directly relates to earning rental income. Second, you must have proof of the expenditure to claim a deduction.

Understanding these two pillars—apportionment and robust record-keeping—is non-negotiable for any property investor. Adherence protects you in the event of an ATO review and ensures all your claims are legitimate.

The Principle of Apportionment

Apportionment is the process of dividing an expense between its private and income-producing use. You can only claim the part that helps generate rental income. This is essential in any situation where there is mixed use.

Consider these common scenarios:

Mixed-Use Loans: If you have an investment loan with a redraw facility and you redraw $20,000 for a private purpose (e.g., a new car), that portion of the loan is now private. You can no longer claim 100% of the loan interest. You must calculate the percentage of the loan that remains for the investment and only claim the interest on that portion.

Holiday Homes: If you own a holiday home that is rented out for 20 weeks of the year and used personally or left vacant for the remaining 32 weeks, you must apportion annual expenses. For costs like council rates and insurance, you could only claim the portion relating to the 20 weeks it was available for rent (i.e., 20/52 or approximately 38%).

ATO-Compliant Record-Keeping

The ATO's stance is unequivocal: no receipt, no deduction. Meticulous record-keeping is your primary defence during an audit and the only way to substantiate your claims. Inadequate records are a major compliance red flag and can lead to denied deductions and penalties.

Essential Documents to Retain

Your records must provide a clear audit trail of your income and expenses.

Checklist of Mandatory Records:

Proof of Income: Rental income statements from your property manager and bank statements confirming receipt of rent.

Proof of Expenses: All receipts, tax invoices, and bank or credit card statements for every claimed expense.

Loan Documents: Bank statements clearly itemising the interest charged on the investment loan.

Purchase and Sale Records: The contract of sale and all associated conveyancing documents are vital for calculating your cost base for Capital Gains Tax (CGT) purposes.

Asset Records: Invoices for the purchase of depreciable assets and any capital works reports from a quantity surveyor.

Under ATO regulations, you must keep these records for at least five years from the date you lodge your tax return. For capital costs related to acquiring or selling the property, records must be kept for five years after the tax return reporting the CGT event is lodged.

Implementing a simple digital filing system, such as dedicated cloud folders or a spreadsheet, is highly effective. Good organisation is a fundamental practice for successful and compliant property investing.

Frequently Asked Questions (FAQ)

1. Can I claim travel expenses to inspect my rental property?

No. For most individuals investing in residential rental properties, travel expenses incurred to inspect, maintain, or collect rent are not deductible. According to the ATO, this legislation was introduced in 2017. This includes the cost of flights, accommodation, and motor vehicle expenses. An exception may apply if you are carrying on a business of property investing, but this is a high threshold that the average investor does not meet.

2. What deductions can I claim if my property is vacant?

You can continue to claim ongoing expenses—such as loan interest, council rates, insurance, and strata fees—during periods of vacancy. However, the property must be genuinely available for rent. The ATO defines this as actively advertising the property at a fair market rate and being prepared to rent it to a suitable tenant. If you cease advertising, use it for personal purposes, or set the rent at an uncommercial rate, it is no longer considered genuinely available, and deductions for that period cannot be claimed.

3. What is negative gearing?

Negative gearing occurs when the deductible expenses for your rental property exceed the rental income it generates in a financial year, resulting in a net rental loss. Under Australian tax law, this net rental loss can be offset against your other assessable income (such as your salary), reducing your overall taxable income and, consequently, your tax liability. This strategy is often used by investors anticipating capital growth over the long term. Understanding its interaction with capital gains and rental property is crucial.

4. Can I claim my entire home loan repayment?

No. This is a common and significant error that the ATO actively monitors. A loan repayment consists of two components, only one of which is deductible:

Interest: The cost of borrowing the funds. This is deductible.

Principal: The portion of the repayment that reduces the loan balance. This is a capital expense and is not deductible. Your loan statements will clearly separate the interest charged, and this is the only figure you can claim.

Summary: Key Takeaways for Tax Success

Achieving compliance and optimising the tax effectiveness of your rental property hinges on several core principles. Use this as a final checklist before preparing your tax return to ensure you meet your obligations and maximise your legitimate returns.

Golden Rules for Rental Deductions

Classify Expenses Correctly: You must accurately differentiate between immediate expenses (e.g., council rates), capital works (the building structure), and depreciating assets (e.g., a new appliance). Incorrect classification is a primary cause of non-compliance.

Apportion for Private Use: If the property or the loan used to acquire it is used for any private purpose, you must accurately apportion all related expenses. Only the portion directly related to generating rental income is deductible.

Maintain Meticulous Records: The ATO requires proof for all claims. You must retain all receipts, invoices, and bank statements for at least five years. Without substantiation, a deduction cannot be claimed.

Stay Informed of Rule Changes: Tax laws evolve. Be aware of key ATO rules, such as the disallowance of travel expenses for residential rentals and the specific regulations for depreciating second-hand assets.

While this guide provides a solid foundation, Australian tax law is complex and subject to change. Navigating it without professional guidance can be stressful and may expose you to financial risk.

To ensure full ATO compliance and implement a tax strategy tailored to your specific circumstances, seeking professional advice is essential.

Contact Baron Tax and Accounting to speak with an expert dedicated to property investment taxation. We can help you achieve your investment goals while ensuring you claim every legitimate deduction available.

Baron Tax and Accounting Website: https://www.baronaccounting.com Email: info@baronaccounting.com Phone: +61 1300 087 213

Comments