How to Calculate Franking Credits: An Australian Guide for Investors

- Jan 15

- 8 min read

Receiving a dividend payment is a great return on your investment, but many investors don't realise there's a crucial step before simply adding the cash to their income: calculating the franking credit attached to it. Understanding this process is vital for accurately reporting your income to the Australian Taxation Office (ATO) and ensuring you don't pay more tax than necessary.

This guide will walk you through the formulas, provide practical examples, and explain why mastering this calculation matters. Getting it wrong can lead to missed tax refunds or incorrect tax assessments. The ATO's dividend imputation system is designed to prevent double taxation on company profits, and franking credits are the key mechanism. Failing to claim them correctly means you could be voluntarily overpaying tax, while incorrect reporting can attract compliance scrutiny and potential penalties.

At Baron Tax & Accounting in Brisbane, we frequently observe clients, particularly those new to investing or managing their own SMSF, who only declare the cash dividend received. This common oversight means they miss out on claiming the franking credit, effectively leaving a tax refund unclaimed. We recently assisted a Brisbane-based retiree who had been under-claiming for years, resulting in a significant amended return once the grossed-up dividends were correctly reported.

What Are Franking Credits and Why Do They Matter?

Franking credits are the cornerstone of Australia’s dividend imputation system. The system’s primary goal is to prevent company profits from being taxed twice—first at the corporate level and again in the hands of the shareholder.

A franking credit is a tax credit passed on to shareholders. It represents the income tax the company has already paid on the profits used to fund your dividend. When you receive a franked dividend, you can use this credit to reduce your personal income tax liability.

This system provides significant benefits for Australian investors:

Avoids Double Taxation: Ensures that company profits distributed as dividends are taxed only once, at the shareholder's marginal tax rate.

Reduces Taxable Income: The credit directly reduces the tax you owe on all your income, not just the dividend.

Potential for a Cash Refund: If your personal tax rate is lower than the company's tax rate, the ATO will refund the difference in cash.

For a deeper dive into the fundamentals, our guide on what are franking credits provides more context.

The Step-by-Step Guide to Calculating Franking Credits

Calculating franking credits involves a two-step process: determining the franking credit amount and then "grossing up" your dividend. This grossed-up amount is what the Australian Taxation Office (ATO) considers your true assessable income from that dividend.

Step 1: Calculate the Franking Credit

Your dividend statement is the primary source of information. It will specify the dividend amount and the company's tax rate (either 30% or 25%).

The official ATO formula is:Franking Credit = Dividend Amount × (Company Tax Rate / (1 - Company Tax Rate))

For a company with the standard 30% corporate tax rate, this simplifies to:Franking Credit = Dividend Amount × (0.30 / 0.70)

Alternatively, a quicker method is:Franking Credit = (Dividend Amount / (1 - Company Tax Rate)) - Dividend Amount

Step 2: Determine Your Grossed-Up Dividend

Once you have the franking credit amount, add it back to the cash dividend you received. This total is your assessable dividend income.

Grossed-Up Dividend (Assessable Income) = Cash Dividend Received + Franking Credit

You must declare this grossed-up figure on your tax return. The franking credit is then applied as a tax offset against the tax calculated on your total income.

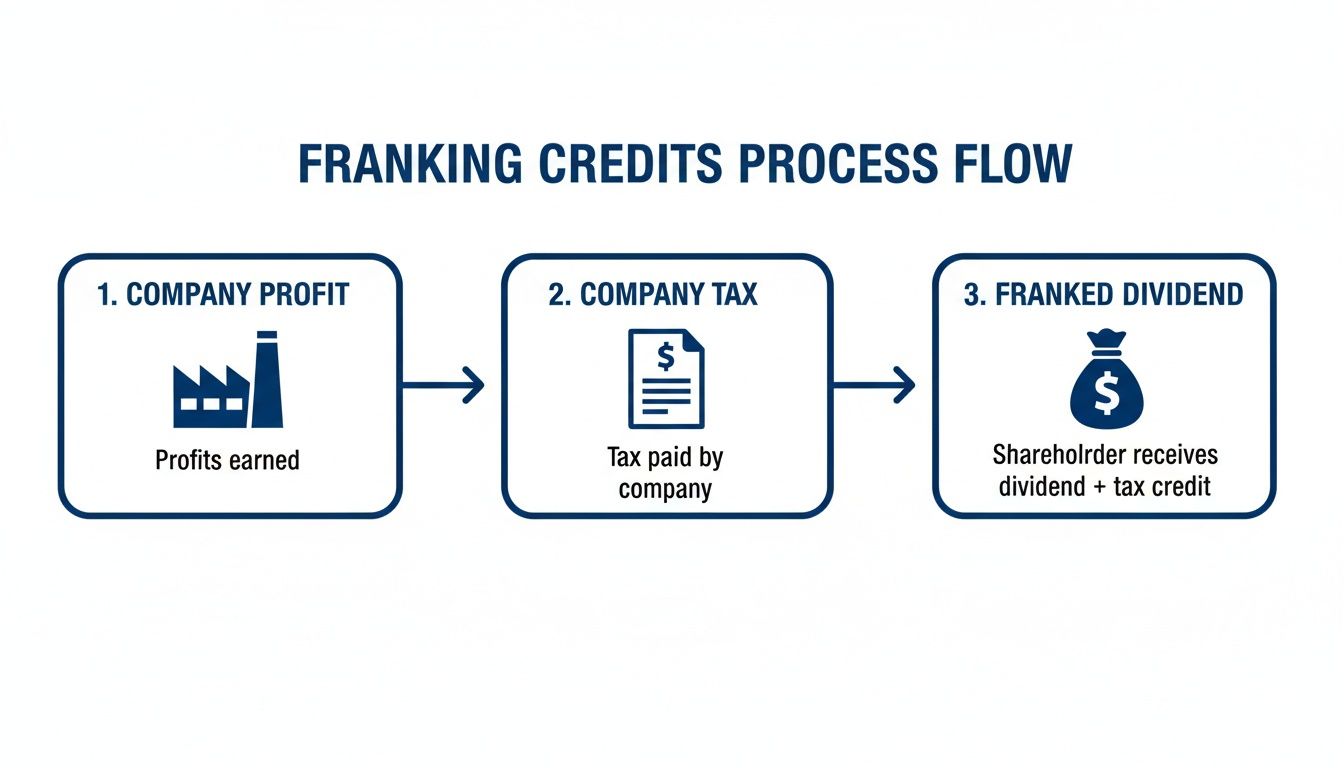

This flowchart illustrates how profits flow from a company to you as a shareholder, showing where the franking credit fits in.

Franking Credit Calculation at a Glance (30% Tax Rate)

This table provides quick calculations for common dividend amounts, demonstrating the franking credit and the total grossed-up dividend to be declared.

Cash Dividend Received | Franking Credit Calculation | Franking Credit Amount | Grossed-Up Dividend (Assessable Income) |

|---|---|---|---|

$700 | $700 × (0.30 / 0.70) | $300 | $1,000 |

$1,400 | $1,400 × (0.30 / 0.70) | $600 | $2,000 |

$3,500 | $3,500 × (0.30 / 0.70) | $1,500 | $5,000 |

$7,000 | $7,000 × (0.30 / 0.70) | $3,000 | $10,000 |

As you can see, the franking credit effectively "tops up" your cash dividend to its pre-tax value. This grossed-up amount is what you’re taxed on, ensuring that the company's tax payment is properly accounted for in your personal tax return.

Practical Examples of Franking Credit Calculations

Theory and formulas become clearer with real-world application. The impact of franking credits on your tax liability varies significantly based on your personal tax rate and the entity receiving the dividend.

Let's explore common scenarios for individuals, small businesses, and super funds.

Example 1: Individual Investor

An investor, Alex, receives a fully franked cash dividend of $700 from a company with a 30% corporate tax rate.

Calculate Franking Credit: $700 × (0.30 / 0.70) = $300

Calculate Gross-Up Dividend: $700 (Cash) + $300 (Credit) = $1,000

Alex must declare $1,000 as assessable income. The final tax outcome depends on Alex's marginal tax rate.

If Alex's Tax Rate is 19%: * Tax on dividend: $1,000 × 19% = $190 * Apply franking credit: $190 (Tax) - $300 (Credit) = -$110 * Result: Alex receives a $110 cash refund from the ATO.

If Alex's Tax Rate is 37%: * Tax on dividend: $1,000 × 37% = $370 * Apply franking credit: $370 (Tax) - $300 (Credit) = $70 * Result: Alex has an additional $70 tax to pay. The franking credit has reduced the tax liability from $370 to $70.

Example 2: Small Business (Company)

A small proprietary limited company receives a cash dividend of $5,000 that is 50% franked. The paying company has a corporate tax rate of 30%.

Isolate the Franked Portion: $5,000 × 50% = $2,500. The remaining $2,500 is unfranked.

Calculate Franking Credit (on franked portion only): $2,500 × (0.30 / 0.70) = $1,071.43

Calculate Gross-Up Dividend: $5,000 (Cash) + $1,071.43 (Credit) = $6,071.43

The company must report $6,071.43 as assessable income. If the company is a small business entity taxed at 25%:

Tax on income: $6,071.43 × 25% = $1,517.86

Apply franking credit: $1,517.86 - $1,071.43 = $446.43

Result: The company owes $446.43 in tax on this dividend income.

Example 3: Self-Managed Super Fund (SMSF)

An SMSF in the accumulation phase (taxed at 15%) receives a fully franked dividend of $14,000 from a company paying tax at 30%.

Calculate Franking Credit: $14,000 × (0.30 / 0.70) = $6,000

Calculate Gross-Up Dividend: $14,000 (Cash) + $6,000 (Credit) = $20,000

The SMSF's tax outcome is:

Tax on income: $20,000 × 15% = $3,000

Apply franking credit: $3,000 (Tax) - $6,000 (Credit) = -$3,000

Result: The SMSF receives a $3,000 cash refund from the ATO, which remains within the fund to boost retirement savings.

How to Report Franking Credits on Your Tax Return

Correctly reporting franking credits to the Australian Taxation Office (ATO) is the final step to ensuring you receive the correct tax offset. All the information you need is on the dividend statement provided by the company.

A Checklist for Reporting Dividends:

Gather All Dividend Statements: Collect statements for every dividend received during the financial year.

Verify Pre-filled Data: If using myTax, the ATO's pre-filling service often populates dividend data. Always cross-reference these figures with your statements to ensure accuracy.

Enter Correct Figures: In your tax return, you will declare: * The franked dividend amount (the cash received). * The franking credit amount.

Confirm Gross-Up: The tax software (like myTax) will automatically add these two figures to calculate your grossed-up assessable income. Confirm this calculation is correct.

Keep Your Records: The ATO requires you to keep all dividend statements for at least five years after you lodge your return as proof of your claims. Our guide on how to file taxes covers this and other reporting requirements.

FAQ: Answering Your Top Franking Credit Questions

Here are answers to some of the most common questions about franking credits, based on ATO regulations.

1. What is the difference between a fully franked and a partially franked dividend?

A fully franked dividend means the company has paid the full corporate tax rate (e.g., 30%) on the profit being distributed. A partially franked dividend means the company has only paid tax on a portion of that profit, so the attached franking credit is smaller. You must declare the unfranked portion as regular income without any credit.

2. What happens if my tax rate is lower than the company's?

This is a key benefit of the system. If your marginal tax rate is lower than the company's tax rate, the franking credit will first reduce your tax liability to zero. Any remaining excess credit is then refunded to you in cash by the ATO. This is common for low-income earners, retirees, and super funds.

3. Do I still need to report unfranked dividends?

Yes. You must declare the full amount of any unfranked dividends as assessable income on your tax return. Since no company tax was paid on this portion of the profit, there is no franking credit to claim. It is taxed at your marginal tax rate, just like salary or bank interest.

4. What is the "45-day holding rule"?

To be eligible to claim franking credits, the ATO requires you to have held the shares "at risk" for a continuous period of at least 45 days (not including the day of purchase or sale). This rule is an integrity measure to prevent "dividend washing," where shares are bought just before a dividend is paid and sold immediately after to harvest the credit.

According to the ATO, this rule does not apply to individuals whose total franking credit entitlement for the income year is below the $5,000 threshold.

Summary: Key Takeaways for Managing Franking Credits

Correctly managing franking credits is essential for maximising your investment returns and ensuring tax compliance.

The "Gross-Up" is Mandatory: You must add the franking credit to the cash dividend received. This total "grossed-up" amount is your assessable income.

Your Dividend Statement is Key: This document contains all the necessary information: the cash dividend, the franking credit amount, and the company tax rate (30% or 25%). Always use the rate specified.

Eligibility Rules Apply: The 45-day holding rule is a critical integrity measure. You must hold shares for at least 45 continuous days (excluding buy/sell days) to claim the credit, unless your total annual credits are less than $5,000.

The Outcome Depends on Your Tax Rate: Your marginal tax rate determines the final result—a tax refund, no change, or additional tax payable.

Need Professional Help With Your Franking Credits?

While this guide covers the core principles, individual tax situations can be complex. Dividend income interacts with other investments, business structures, and superannuation strategies. Getting personalised advice ensures you are compliant and optimising your tax position.

A qualified tax professional can help you navigate:

How your marginal tax rate affects your dividend income.

Compliance with eligibility rules like the 45-day holding period, especially if your claims exceed $5,000.

The interaction between dividends and other income types, such as capital gains.

Optimising outcomes for structures like SMSFs, where franking credits are particularly valuable.

For more on how professional advice can help, see our article on dedicated tax specialists.

The team at Baron Tax & Accounting provides clear, practical advice to help you manage your investment income with confidence.

Contact Us

Get in touch with Baron Tax and Accounting for a confidential chat about your investment income and tax needs.

Website: https://www.baronaccounting.com

Email: info@baronaccounting.com

Phone: +61 1300 087 213

Whatsapp: 0450468318

Line: Barontax

Comments